Economics explained

Category:

Market structures

Barriers to entry

The secret to scoring awesome grades in economics is to have corresponding awesome notes.

A common pitfall for students is to lose themselves in a sea of notes: personal notes, teacher notes, online notes textbooks, etc... This happens when one has too many sources to revise from! Why not solve this problem by having one reliable source of notes? This is where we can help.

What makes TooLazyToStudy notes different?

Our notes:

-

are clear and concise and relevant

-

is set in an engaging template to facilitate memorisation

-

cover all the important topics in the O level, AS level and A level syllabus

-

are editable, feel free to make additions or to rephrase sentences in your own words!

Looking for live explanations of these notes? Enrol now for FREE tuition!

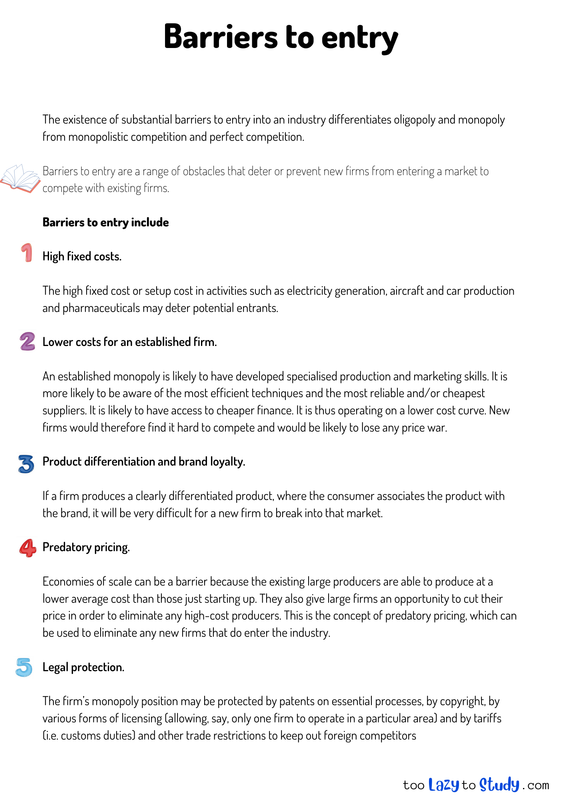

The existence of substantial barriers to entry into an industry differentiates oligopoly and monopoly from monopolistic competition and perfect competition.

Barriers to entry are a range of obstacles that deter or prevent new firms from entering a market to compete with existing firms.

Barriers to entry include

High fixed costs.

The high fixed cost or setup cost in activities such as electricity generation, aircraft and car production and pharmaceuticals may deter potential entrants.

Lower costs for an established firm.

An established monopoly is likely to have developed specialised production and marketing skills. It is more likely to be aware of the most efficient techniques and the most reliable and/or cheapest suppliers. It is likely to have access to cheaper finance. It is thus operating on a lower cost curve. New firms would therefore find it hard to compete and would be likely to lose any price war.

Product differentiation and brand loyalty.

If a firm produces a clearly differentiated product, where the consumer associates the product with the brand, it will be very difficult for a new firm to break into that market.

Predatory pricing.

Economies of scale can be a barrier because the existing large producers are able to produce at a lower average cost than those just starting up. They also give large firms an opportunity to cut their price in order to eliminate any high-cost producers. This is the concept of predatory pricing, which can be used to eliminate any new firms that do enter the industry.

Legal protection.

The firm’s monopoly position may be protected by patents on essential processes, by copyright, by various forms of licensing (allowing, say, only one firm to operate in a particular area) and by tariffs (i.e. customs duties) and other trade restrictions to keep out foreign competitors